It was nice to have a long weekend to rest up after the absolute barrage of economic data and news that came out last week before the holiday.

It was frankly a lot of work to process, but I powered through knowing that procrastination was all but impossible given the imminent and unavoidable Thursday/Friday Thanksgiving food coma. There may have only been three people at the dinner table, but it felt like I made enough food for thirty.

Here’s to stretchy pants and no guests.

Anyway, lots of data to get through so I’ll jump right in. First off, and most importantly, jobs data continues to disappoint as initial claims rose week-on-week, coming in well above expectations at 778,000 people.

Source: Bloomberg

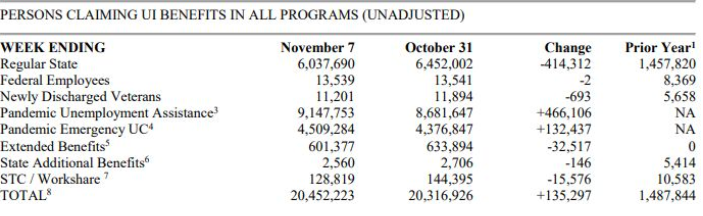

And while traditional continuing claims were down pretty sizably, that was more than offset by an increase in Pandemic Unemployment Assistance (PUA). As a result, the total number of people receiving some kind of unemployment benefits the week of November 7th rose by 135,000 to 20.45 million.

Source: Department of Labor

Emergency benefits are slated to expire at the end of the year and many claimants have exhausted their maximum state-level benefits. As a result, we’re starting to see this trend play out in personal income, which unexpectedly fell -0.7% in October. That is likely to eventually infringe on personal spending, which still grew in November, but by a smaller amount in line with expectations.

Source: Bloomberg

I keep emphasizing this topic because consumer spending comprises roughly 70% of US GDP. So if someone doesn’t have income, it stands to reason that they would be spending less, and that should theoretically push GDP lower.

And although Q3 GDP rose 33.1% on the quarter, in line with expectations, we’re still not back to the absolute value achieved in Q4 of last year.

Source: Bloomberg

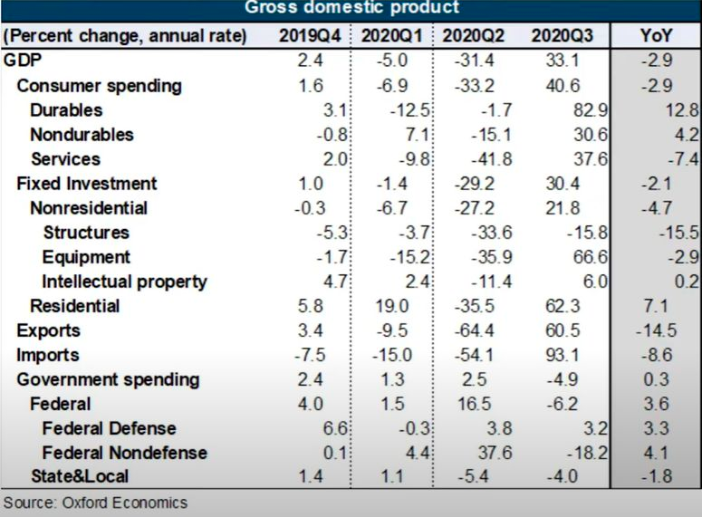

And the macroeconomic themes we have discussed in these pages are very much at work, with all parts of the GDP formula down year-on-year except government spending… naturally.

Source: Bloomberg

That means that if we want the economy to get better, Congress needs to pass stimulus ASAP.

Well believe it or not, that is back on the table now, as a bipartisan group of Senators just introduced a “skinny” version of stimulus valued at US$908 billion. It’s unclear whether or not it can get broad support, but at this point, with evictions looming at year’s end, we’ll take what we can get.

It’s been speculated that Biden’s nomination of former Fed chair Janet Yellen to be the country’s next Secretary of the Treasury is a signal that fiscal policy will be easier and more coordinated with actions put forth by the Federal Reserve.

Any additional stimulus is welcome, as it not only shores up the economy, but also our stakes in Proshares UltraGold (NYSEArca: UGL) and Proshares UltraSilver (NYSEArca: AGQ), which got torched last week on low volume, briefly pulling down below respective support at $60 and $40, and triggering another ¼ stake deployment in each as per my commentary back on November 18th.

Both came roaring back today as the yellow metal closed above the critical $1800 per troy ounce mark and more importantly, closed above its 200-day moving average.

Source: Bloomberg

To finance these moves, we can go ahead and sell our stake in the former Fortress Valley Acquisition Company (FVAC) – which I recommended picking up back on Election Day. The company finally closed its merger and transitioned into MP Materials (NYSE: MP) last week and has since doubled from its recent lows.

We’ll probably jump back in at a later time, but it seems to have run too far, too fast at the moment.

Europe Likely to Get More Stimulus from ECB

I think the biggest news, however, doesn’t directly involve the United States.

In the European Central Bank’s Forum just a couple of weeks ago, ECB President Christine Lagarde said that “while the latest news on a vaccine looks encouraging, we could still face recurring cycles of accelerating viral spread and tightening restrictions until widespread immunity is achieved. So, the recovery may not be linear, but rather unsteady, stop-start and contingent on the pace of vaccine rollout.”

We’ve already seen some evidence of this, as France’s economy was recently shut down to prevent spread of COVID-19. Although the lockdown is set to be lifted on December 15th, French President Macron is keeping bars and restaurants closed through Christmas as part of a 3-stage easing over the next two months.

Because of the resulting hit to GDP, the European Central Bank strongly suggested at their October meeting that more stimulus was to come by year’s end.

And Lagarde herself noted the other day that, “while all options are on the table, the PEPP (Pandemic Emergency Purchase Program) and TLTROs (targeted longer-term refinancing operations) have proven their effectiveness in the current environment and can be dynamically adjusted to react to how the pandemic evolves. They are therefore likely to remain the main tools for adjusting our monetary policy.”

Given that there are likely a whole bunch of Euro about to be printed – and that same Euro just made fresh 2-year highs versus the US Dollar – it stands to reason that this move will make a strong reversal, whether it’s before the ECB meeting or afterward.

Source: Bloomberg

And although some of the large non-commercial longs in the Euro have come off, there are still a whole lot out there.

Source: Hedgopia

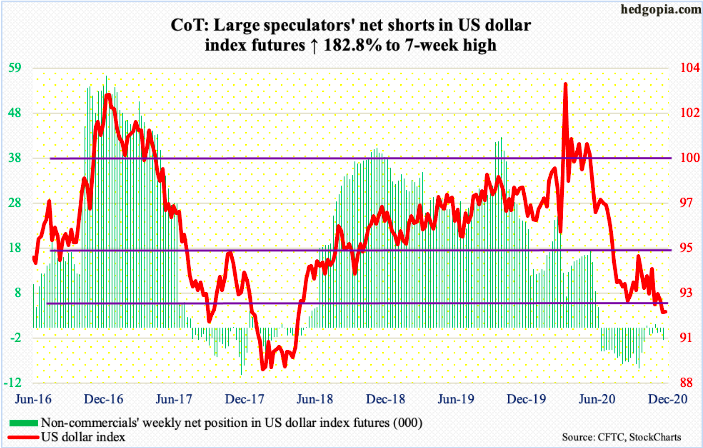

It’s sort of the same story for the dollar bears as well. Although large speculative short bets have backed off over the last month or so, the market is still net short.

Source: Hedgopia

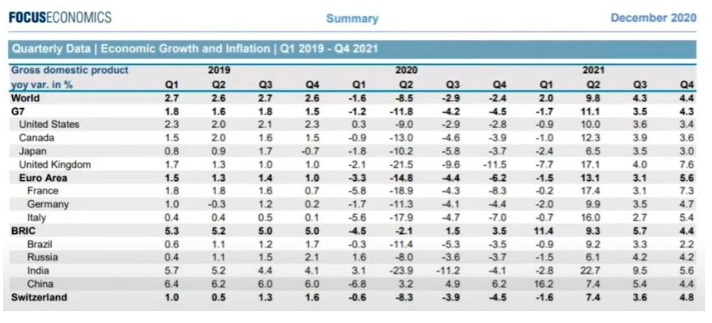

Moreover, economic forecasters are starting to turn more bearish on the Eurozone in general, as it is clearly mired in a deep recession. Even powerhouse economies like Germany are projected to post year-on-year declines in GDP through Q2 of next year. And those that have been hit harder, like France and Italy, are much worse.

Source: Hedgopia

This is a deep hole to crawl out of, and even with the stimulus, I’m not convinced Europe bounces back quickly. As such, I want to add ½ tranche to the position in ProShares UltraShort Euro (NYSEArca: EUO) to hold through the meeting on December 10th.

If we get a significant pullback, then we can hold for a bit. Meanwhile if nothing happens to the currency market, then we’ll just close it out.

But given how much Euro they’ll likely have to print to get those economies back on track, it would be hard to believe the currency doesn’t get significantly debased.

And if it doesn’t, then we should just all go outside and make a bonfire out of our economics textbooks.

All the best,

Matt Warder

Venture Society

This article is supplied courtesy of VentureSociety.com